A comparative market analysis (CMA) in real estate is a data-driven report that estimates a property’s value based on recently sold comparable properties in the same area. In 2026, with median home prices shifting across nearly every U.S. market, a well-built CMA is one of the most powerful tools an agent can bring to a listing appointment or buyer consultation. It gives sellers a defensible price, gives buyers negotiating confidence, and gives you, the agent, a clear path to winning the business.

This guide walks you through exactly what a CMA is, how to build one in six steps, how to present it so clients say yes, and the mistakes that cost agents listings. Whether you are preparing your first CMA or refining a process you have used for years, the framework below will sharpen your pricing accuracy and your conversion rate.

Find It Fast

Key Takeaways

- A CMA in real estate estimates a property’s market value using recently sold comparable properties, active listings, and pending sales in the same area.

- A CMA is not a formal appraisal. Agents prepare CMAs using market data and local knowledge, while licensed appraisers conduct appraisals for lenders.

- The six-step CMA process covers property data collection, comp selection, comparison, price adjustments, data consolidation, and client presentation.

- Selecting four to six strong comps sold within the last three to six months is the single most important factor in CMA accuracy.

- How you present the CMA matters as much as the data inside it. A clear, visual, branded presentation builds trust and wins listings.

- Common CMA mistakes include using too few comps, ignoring active and pending listings, and skipping price adjustments for property differences.

What Is a Comparative Market Analysis (CMA) in Real Estate?

A comparative market analysis is a report that estimates a property’s market value by examining the sale prices of similar properties in the same neighborhood or area. The CMA evaluates factors such as square footage, lot size, bedroom and bathroom count, condition, location, and recent upgrades to arrive at a recommended price range. Buyers, sellers, and agents all rely on CMAs to make informed pricing decisions. The term “Realtor” refers to a member of the National Association of Realtors (NAR), and this guide uses “Realtor” and “agent” interchangeably. NAR provides guidance on pricing strategy and CMA methodology that agents can reference when structuring their analysis (NAR Research and Statistics, 2026).

Why Agents Need a CMA in 2026

A real estate market analysis benefits every party in a transaction, but it benefits the agent most of all. A strong CMA is your proof of competence. It shows a seller you understand their neighborhood, their property, and the pricing dynamics that will determine how fast and how profitably their home sells. It shows a buyer exactly where the negotiation leverage sits. For sellers, the CMA answers the question they care about most: “What is my home worth right now?” It replaces guesswork with data. For buyers, a CMA helps them set a realistic budget, understand whether an asking price is fair, and adjust their return expectations if the purchase is an investment. For agents, a CMA makes the pricing conversation specific and defensible rather than subjective.

“We were going to price it where it needs to sell, right at the number.”

— Matt Breitenbach, Real Estate Agent

That mindset is the difference between an agent who wins the listing and an agent who loses it to someone willing to “try a higher price.” When you walk into a listing appointment with a CMA that shows exactly why a property should be priced at a specific number, backed by sold comps and adjusted for differences, you remove emotion from the conversation and replace it with evidence. That is how you earn trust, and trust is how you earn the signature on the listing agreement.

How To Conduct a CMA in Real Estate: 6 Steps

Step 1: Gather data on the subject property

Build a thorough database of information about the property you are pricing. The listing sheet is a starting point, but go further. Pull the current tax rate, historical improvement permits, and ownership records from your local government administrative offices. Research how the property’s price has moved through past market cycles. Has it tracked with neighborhood trends or deviated from them? Has ownership changed frequently, and if so, why? Collect the following data points for the subject property:

- Year built

- Total square footage

- Number of bedrooms and bathrooms

- Location details (school district, walkability, proximity to transit)

- Lot acreage

- Architectural style

- Interior finish quality (countertops, flooring, fixtures)

- Amenities (pool, fireplace, garage, finished basement)

- Documented improvements and renovation permits

- Previous year’s property tax bill

- Overall condition (roof age, HVAC age, foundation status)

- Full sales and pricing history with notes on any deviations from market trends

The more detail you capture here, the stronger your comp adjustments will be in later steps. Do not skip this step or rush through it. The data you collect now is the foundation of every pricing decision that follows.

Step 2: Select comparable properties (comps)

Identifying four to six comparable properties is the most consequential step in the CMA process. Your comps are the evidence behind your price recommendation. If the comps are weak, the entire analysis falls apart. Start with recently sold properties in the same neighborhood or a neighborhood with similar characteristics. The closer the match to your subject property, the more reliable your price estimate will be. Use these criteria to filter your comps:

- Sold within the last three to six months (extend to 12 months only in low-transaction markets)

- Located within a half-mile to one mile of the subject property, or in a comparable neighborhood

- Similar in square footage, bedroom count, bathroom count, and lot size

- Similar in condition and age

- Sold through arm’s-length transactions (not foreclosures, short sales, or family transfers unless those dominate the local market)

Do not stop at sold comps. Also pull data on active listings and pending (under-contract) properties. Active listings show you what the competition looks like right now. Pending listings reveal what buyers are actually willing to pay. Together, these three categories give you a full picture of supply, demand, and pricing momentum in the local market. Pull your comp data from the Multiple Listing Service (MLS), which is the database where agents share listing information. After the first mention, this guide refers to it as the MLS. If the subject property has features that are hard to match, such as a guest house, waterfront access, or a commercial zoning overlay, you may need to widen your search radius or look at a longer time window. Finding and assessing accurate comps is a skill that improves with practice and local knowledge.

Step 3: Compare your property with the comps

Start by analyzing the subject property’s historical value. Look at what it last sold for, when that sale occurred, and how the broader market has moved since then. Use that context to form an initial estimate of where the property sits in the 2026 market.

Start by analyzing the subject property’s historical value. Look at what it last sold for, when that sale occurred, and how the broader market has moved since then. Use that context to form an initial estimate of where the property sits in the 2026 market.

Next, compare the sold prices of your comps. Line them up side by side and note the price per square foot for each. If the market has been volatile, tighten your comp window to three to six months to avoid stale data. Then assess the active and pending listings. How are similar properties priced right now? How long have they been on the market? Properties that have been sitting for 60 or 90 days may signal overpricing, which is useful context for your recommendation.

One of the biggest differences between your CMA and an automated estimate is your local knowledge. You know that a property might command a premium because of the school district, a new commercial development nearby, or a planned transit stop. Factor that intelligence into your analysis. Finally, create a price range by ranking all of your data points from lowest to highest. This range becomes the starting point for your recommended list price.

Step 4: Adjust for differences between the subject property and comps

No two properties are identical. Your comps will differ from the subject property in bedroom count, bathroom count, lot size, condition, upgrades, or amenities. Your job is to make dollar adjustments that account for those differences so the comparison is as close to apples-to-apples as possible. Here is how adjustments work in practice. If a comp has one fewer bedroom than the subject property, you add value to the comp’s sale price to reflect what it would have sold for with that extra bedroom. If the comp has a renovated kitchen and the subject property does not, you subtract value from the comp’s sale price.

| Adjustment Factor | Subject Property Has More | Subject Property Has Less |

| Bedrooms | Add value to comp price | Subtract value from comp price |

| Bathrooms | Add value to comp price | Subtract value from comp price |

| Garage spaces | Add value to comp price | Subtract value from comp price |

| Finished basement | Add value to comp price | Subtract value from comp price |

| Updated kitchen or bathrooms | Add value to comp price | Subtract value from comp price |

| Lot size (significantly larger or smaller) | Add value to comp price | Subtract value from comp price |

The dollar amounts for each adjustment come from your local market knowledge and MLS data on how specific features affect sale prices in that neighborhood. This step requires judgment, and it is where experienced agents separate themselves from newer ones. The goal is to make every comp tell you what the subject property is worth, even though no comp is a perfect match.

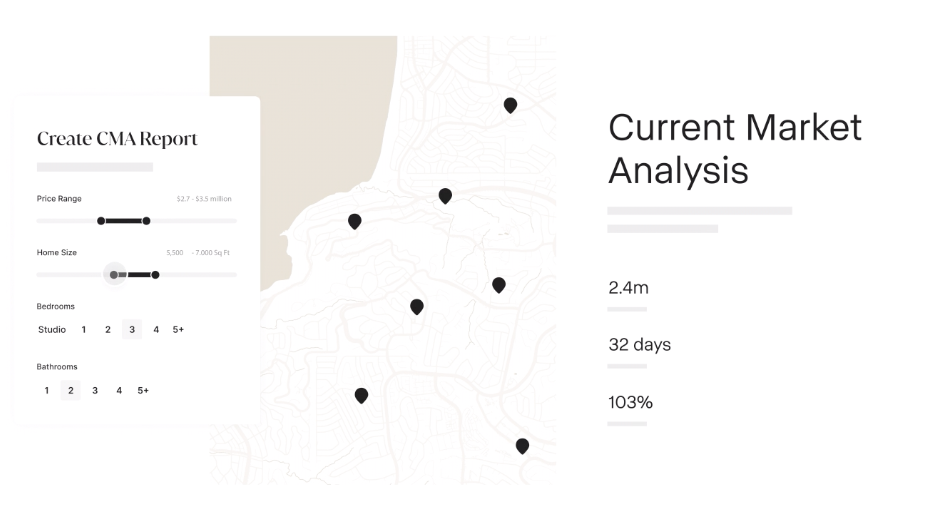

Step 5: Consolidate your data and set a price range

After adjustments, calculate the average adjusted price per square foot across all of your comps. Multiply that figure by the subject property’s square footage to arrive at an estimated value.

Then set a price range, with the low end reflecting a conservative, quick-sale price and the high end reflecting a more aggressive position. Present the range to your client, not a single number. The range gives sellers a framework for understanding the trade-off between pricing aggressively (faster sale, more showings, possible multiple offers) and pricing at the top of the range (longer days on market, fewer showings, risk of price reductions).

Because a CMA relies on an agent’s judgment and local expertise, two agents can produce slightly different CMAs for the same property. That is normal. The market will ultimately determine the final sale price. Your CMA is the tool that gets your client as close to that number as possible before the first showing.

Step 6: Present your CMA to the client

The data is only half the battle. How you present the CMA determines whether the client trusts your recommendation and signs the listing agreement. A disorganized spreadsheet or a wall of numbers will lose the room. A clear, visual, branded presentation will win it. Structure your CMA presentation with these sections in order:

The data is only half the battle. How you present the CMA determines whether the client trusts your recommendation and signs the listing agreement. A disorganized spreadsheet or a wall of numbers will lose the room. A clear, visual, branded presentation will win it. Structure your CMA presentation with these sections in order:

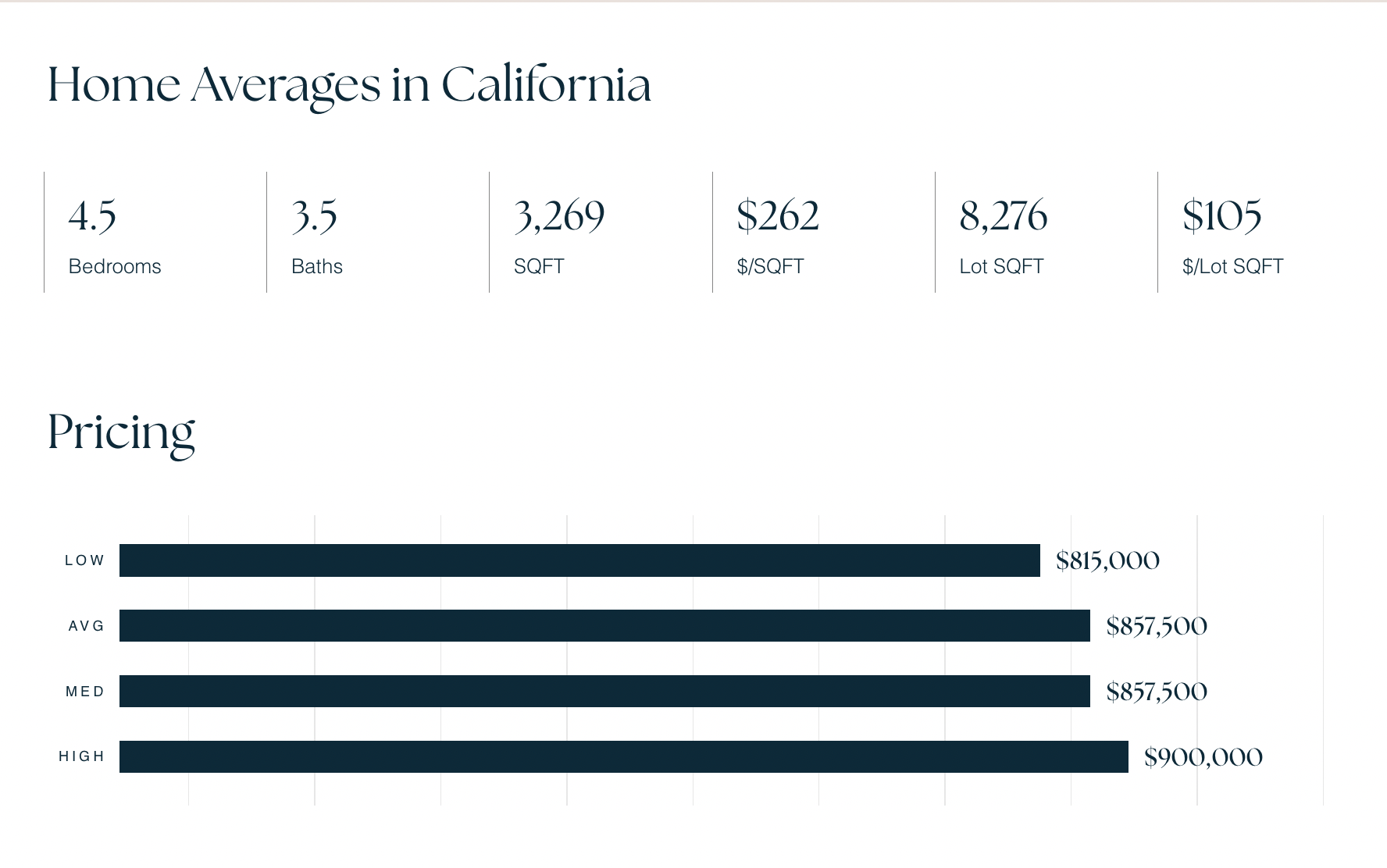

- Market overview: Start with a brief snapshot of the local market. Include median sale price, average days on market, and inventory levels for the neighborhood. This sets the stage.

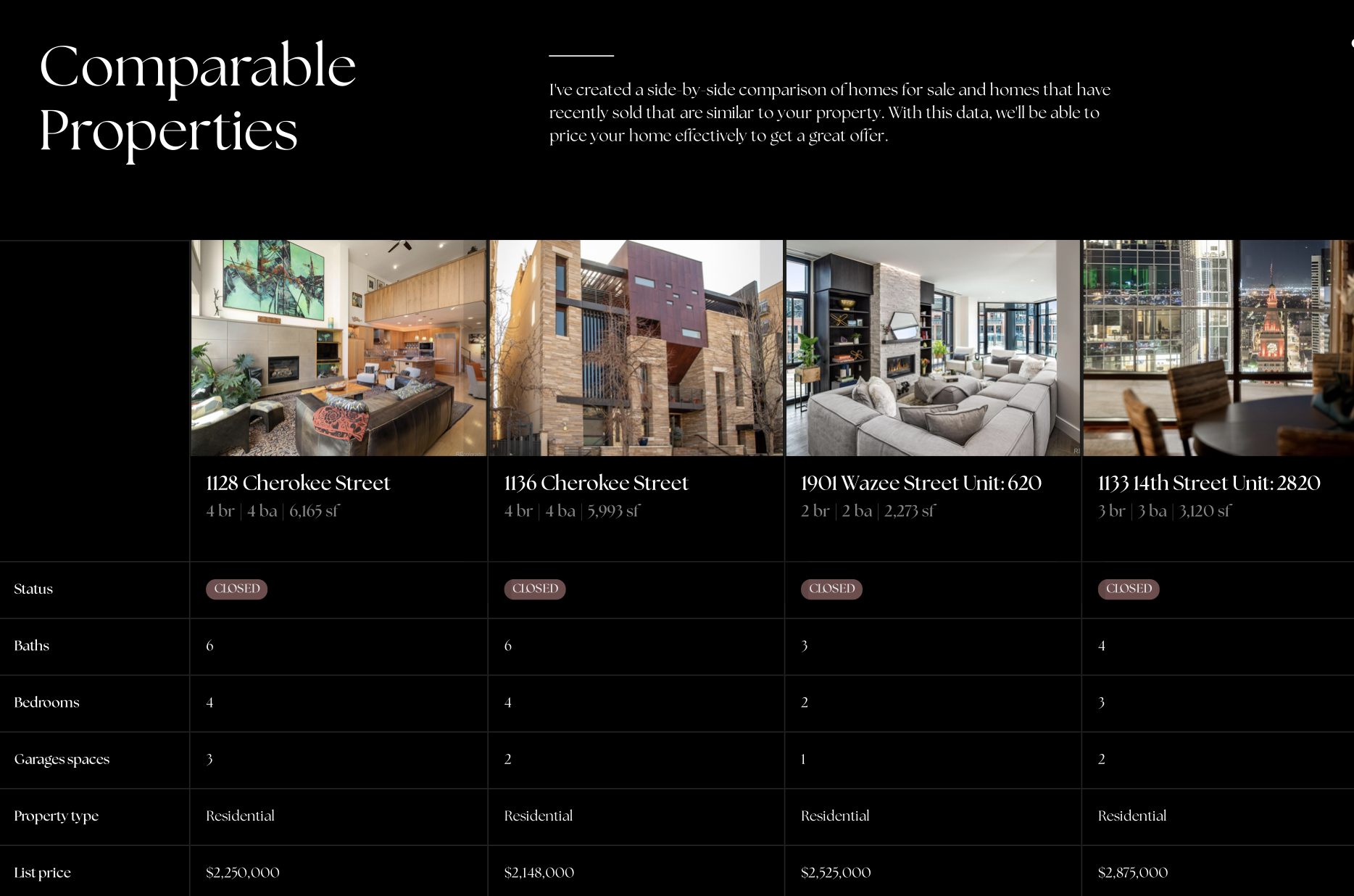

- Subject property summary: Show the property’s key features, photos, and any upgrades or condition notes. Confirm the details with the client to build rapport and show you have done your homework.

- Comp breakdown: Display each comp with a photo, address, sale price, price per square foot, days on market, and the adjustments you made. Use a side-by-side layout so the client can see the comparison at a glance.

- Active and pending listings: Show what the competition looks like right now. This helps the client understand where their property fits in the current landscape.

- Recommended price range: Present your range with a clear explanation of why you recommend a specific list price within that range. Walk the client through the trade-offs of pricing high versus pricing at market.

- Your marketing plan: Close with how you plan to market the property. This is where you connect the pricing strategy to the listing presentation and show the client the full picture.

“It shows that you’re going above and beyond to market their home, to make it look great, and to bring in the best offers.”

— Tracy Tutor, Real Estate Agent

That is exactly the impression a polished CMA presentation creates. When a seller sees a branded, visual report that walks them through the data with clarity and confidence, they see an agent who takes their business seriously. Use a digital presentation tool to build your CMA so it is easy to share, easy to update, and consistent with your brand. Luxury Presence’s presentation builder pulls data directly from your MLS and formats it into a shareable, branded report that reflects the quality of your service.

CMA vs. Appraisal: What Is the Difference?

A CMA and a formal appraisal both estimate a property’s value, but they serve different purposes and are conducted by different people.

| Factor | CMA | Formal Appraisal |

| Who prepares it | Real estate agent | Licensed, certified appraiser |

| Purpose | Pricing guidance for listing or offer strategy | Property valuation for a lender or insurer |

| Regulation | No licensing requirement | Governed by federal and state appraisal standards |

| Cost to the client | Typically free (provided by the agent) | $300 to $600 or more, paid by the buyer or borrower |

| When it happens | Before listing or before making an offer | After an accepted offer, ordered by the lender |

| Data sources | MLS, public records, agent’s local knowledge | MLS, public records, physical property inspection |

The Appraisal Institute distinguishes a formal appraisal, which is conducted by a licensed appraiser for lender or insurance purposes, from an agent-prepared CMA, which is a market-based pricing tool that does not carry the same regulatory weight (Appraisal Institute, 2026). Both are valuable, but they answer different questions at different stages of the transaction.

Example of a Comparative Market Analysis in 2026

Scenario setup

In 2026, the Cooper family is considering a four-bedroom house with 2,000 square feet, listed at $400,000. They believe the price is too high and ask their agent to conduct a CMA to support a lower offer. Here are the subject property details:

- Four bedrooms, three full bathrooms, and one half-bathroom

- 2,000 square feet on a half-acre lot

- Fireplace, two-car garage, and a fully finished basement

- Good condition with no deferred maintenance

- Located in a neighborhood with many homes of similar size and age

Calculation walkthrough

The agent identifies four comparable properties that sold within the past four months in the same neighborhood. One comp has five bedrooms, no finished basement, and sold for $400,000. The agent adjusts for the differences:

- The extra bedroom in the comp adds roughly $5,000 to its value, so the agent adjusts the comp price down to $395,000 to reflect what it would have sold for with four bedrooms.

- The comp lacks a finished basement, which the subject property has. The agent adds $3,000 to the comp’s adjusted price, bringing it to $398,000.

The agent repeats this process for all four comps. After adjustments, the agent calculates the average price per square foot across all comps and arrives at $190 per square foot. (This figure is illustrative. In practice, agents should derive the price-per-square-foot figure from actual sold comps in the subject property’s specific neighborhood and time window.) Multiplying $190 by the subject property’s 2,000 square feet produces an estimated value of $380,000. Comp prices in this example reflect a mid-2026 market scenario for illustrative purposes. The Coopers now have data to support an offer of $380,000, which is $20,000 below the asking price. Because the offer is grounded in comparable sales, the seller is more likely to take it seriously and engage in a productive negotiation.

Common CMA Mistakes To Avoid

Even experienced agents make errors that weaken their CMA and undermine their pricing recommendation. Here are the most common mistakes and how to avoid them:

- Using too few comps. One or two comps do not give you enough data to establish a reliable price range. Use four to six comps whenever possible.

- Choosing comps that are too old. A comp from 18 months ago may reflect a completely different market. In a shifting 2026 market, prioritize comps from the last three to six months.

- Ignoring active and pending listings. Sold comps tell you where the market was. Active and pending listings tell you where the market is heading. You need both.

- Skipping adjustments. If your comps differ from the subject property in bedrooms, condition, or amenities and you do not adjust, your price estimate will be off.

- Relying on automated estimates alone. AVMs are a starting point, not a finish line. They cannot account for condition, upgrades, or hyperlocal factors that only a local agent knows.

- Presenting raw data without context. A spreadsheet full of numbers does not build trust. Wrap your data in a clear narrative that explains what the numbers mean and why you recommend a specific price.

FAQs

About the author

Kate Evans is a content marketing strategist at Luxury Presence, the leading growth platform for high-performing real estate professionals. She develops data-driven editorial content and supports SEO strategy and brand voice frameworks that help agents attract qualified leads and establish market authority. Her published work covers topics including CRM strategy, social media marketing, and digital growth, supporting thousands of agents in scaling their businesses through modern marketing.